Sustainability

We have an important role to play in creating a more sustainable and inclusive future.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

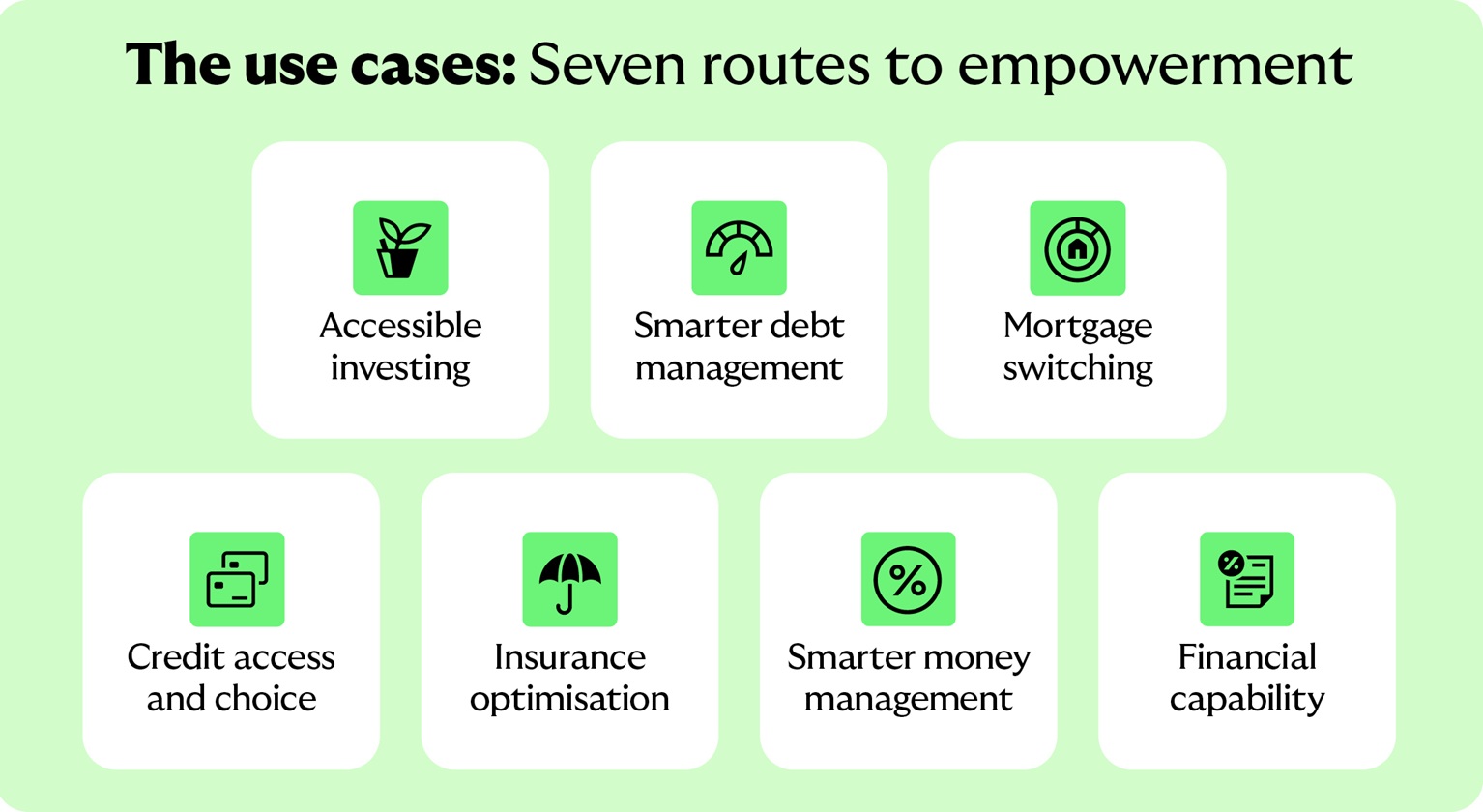

Helping the nation make the most of its finances

What could true financial empowerment unlock for the UK – at scale?

As one of the UK’s largest integrated financial services organisations, we wanted to understand the scale of opportunity that comes from true financial empowerment, enabled by digital transformation.

To explore this, we commissioned Professor John Gathergood, Professor of Financial Economics at the University of Nottingham. Drawing on published academic evidence, nationally representative survey data, and economic modelling, his research answers a key question: if the benefits of digitally-enabled financial empowerment were realised at scale across the UK population, what could be the total value to the nation over the next decade?

"Financial empowerment comes when people have the confidence, tools, knowledge and opportunities to take control of their financial lives and improve their financial wellbeing over time. No financial services provider offers more choice, convenience or reach to make that happen."

"Consumers can achieve financial empowerment by harnessing the latest advances in digital and related technologies, using products and tools which are tailored to their needs, and help them shape the lives they want to lead."

Advances in data, technology, and digital channels enable the financial services industry to support UK consumers by giving them the information, tools, and technology to make better financial choices. Digital transformation empowers consumers by helping them manage their money in ways that are low cost, fast, easy to access, and always-on.

This report sets out how digital transformation can support consumers in seven key areas. These areas span a range of consumer finances – from everyday money management to investing for the longer term; from better access to credit and borrowing, to making sure consumers have the right insurance products. Across these areas, digitally-enabled financial services can help consumers make better decisions at every stage of life.

Digital tools already exist – in people's pockets, embedded in their banking apps – and are continuously developed and improved in ways that can make consumers meaningfully better off.

The evidence, drawn from rigorous academic research and representative survey data, is clear: these tools work and, as digital transformation takes hold, could benefit millions more people. When this next generation of digitally-delivered tools is deployed and adopted at scale, the benefits will be felt across society.

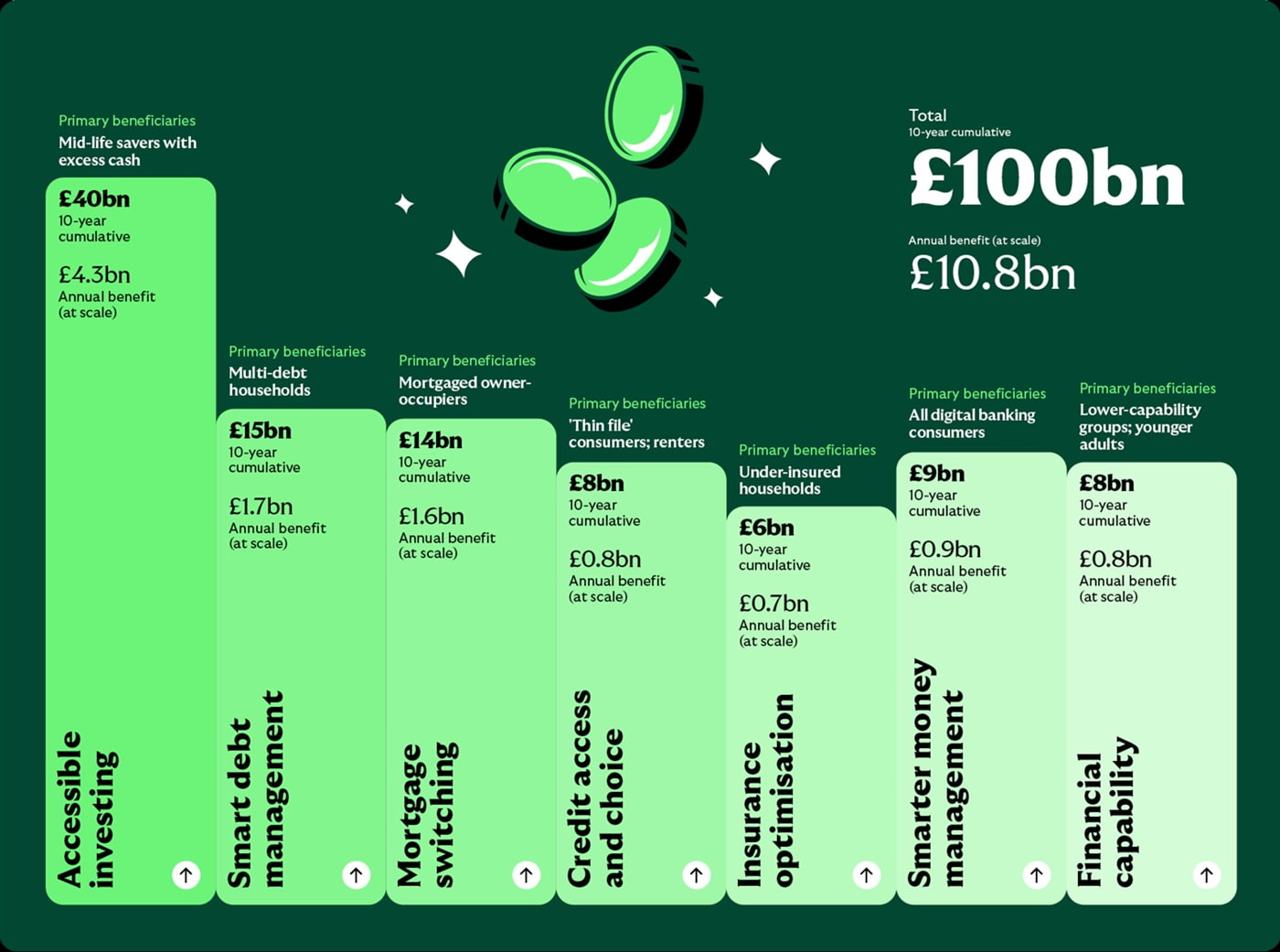

The research indicates that if digital financial empowerment were deployed at scale across the UK population, the cumulative benefit to consumers would reach £100 billion over ten years. This is equivalent to approximately £3,500 per UK household. The impact would be felt across all income groups. Projections show that the benefits are largest among those on lower incomes.

"The benefits to lower income households amass to £31 billion, or approximately 9.2% of household income."

The largest absolute monetary gains – from increased investing, mortgage decisions and higher investment returns – accrue to those with savings. But the largest relative gains – in debt management, credit access, and money management – accrue to lower income households. These households have the most to gain, as digital transformation helps to overcome complexity, frictions, and information gaps in credit and debt markets.

"The benefits to higher income households amass to £69 billion, or approximately 8.2% of household income."

Digital tools can help UK adults move cash savings not ear-marked for short-term needs out of low‑yield accounts and into diversified investment portfolios, achieving materially higher real returns through digitally delivered investment guidance from providers.

A single-view debt dashboard with technology-enabled repayment prompts could enable households holding multiple unsecured products to reduce their interest costs by repaying in the optimal order.

Digital pre-approval and eligibility-checking tools could reduce the friction that leads mortgaged households to remain on uncompetitive rates when better deals become available.

Incorporating alternative data – rent payments, utility bills, Open Banking transaction data – into credit scoring can unlock mainstream credit access for millions of consumers currently excluded by thin-file status.

Transaction data analysis can identify underinsurance gaps and eliminate duplicate or unnecessary premiums, helping households achieve the right coverage at the right cost while ensuring their insurance is right-sized for their needs.

Technology-enabled money management tools can provide proactive, forward-looking cash flow alerts. This helps customers set aside short-term savings for emergencies, save money by cancelling dormant subscriptions, and refine their spending patterns, to avoid costly everyday financial mistakes.

Contextual digital guidance embedded in banking apps at key financial decision-making moments improves outcomes for consumers who wouldn’t otherwise seek or receive financial education.

The aggregated financial benefits from each use case are shown in the graph above. The largest absolute financial gains – from accessible investing to smarter money management – reflect the compounding power of investments deployed more efficiently over time.

However, the largest relative gains, as a proportion of income, accrue to lower-income households through improved debt management, better credit access, and smarter everyday money management.

Together, the seven use cases represent a comprehensive picture of where digital transformation can unlock the most value: from one-time switching events in mortgages and debt consolidation, to continuous and compounding benefits in investment returns.

The projected benefits are achievable with existing or near-term technology and are individually supported by a robust base of published academic and empirical evidence.

Crucially, the seven use cases are non-overlapping: a consumer who benefits from both mortgage switching and accessible investing is capturing two distinct financial gains, and neither is double-counted.

It should be noted that several areas of potential consumer benefit are excluded from this analysis. Savings behaviour (the decision to save versus spend), wealth accumulation beyond the investment returns modelled in use case one (such as through pensions optimisation), and behavioural spillover effects (where improvements in one area of financial management leads to improvements in others) are all outside the scope of this report. Their exclusion contributes to the conservatism of the overall estimate.

The seven use cases are independent in their mechanisms and consumers can benefit from more than one use case. For example, a consumer who benefits from mortgage switching and accessible investing is capturing two distinct financial gains, which aren’t double-counted. The aggregate is therefore additive, summing across the individual use cases with minimal overlap.

The estimates presented throughout this report are intentionally conservative. Uptake rates are calibrated to observed adoption curves for comparable digital financial services, and in most cases represent the lower end of plausible ranges. The use cases are designed to be non-overlapping: where there is potential for a benefit to be captured by more than one use case (for example, between financial capability and investing), explicit overlap adjustments are applied to prevent double-counting.

Certain areas of potential benefit – including savings behaviour, wealth accumulation effects, and broader macroeconomic multipliers – are excluded from the modelling entirely, further reinforcing the conservatism of the headline estimate.

|

Eligible population |

Target uptake |

Beneficiaries |

Avg. annual benefit |

10 year cumulative |

|

|---|---|---|---|---|---|

|

Eligible population Accessible investing |

Target uptake ~18m adults |

Beneficiaries 36% |

Avg. annual benefit 6.5m |

10 year cumulative £660 per person |

£40 billion |

|

Eligible population Smart debt management |

Target uptake ~17m adults |

Beneficiaries 29% |

Avg. annual benefit 5.0m |

10 year cumulative £340 per person |

£15 billion |

|

Eligible population Mortgage switching |

Target uptake ~8m households |

Beneficiaries 25% |

Avg. annual benefit 2.0m |

10 year cumulative £1,600 per household |

£14 billion |

|

Eligible population Credit access and choice |

Target uptake ~5m adults |

Beneficiaries 40% |

Avg. annual benefit 2.0m |

10 year cumulative £390 per person |

£8 billion |

|

Eligible population Insurance optimisation |

Target uptake ~14m households |

Beneficiaries 36% |

Avg. annual benefit 5.0m |

10 year cumulative £138 per household |

£6 billion |

|

Eligible population Smarter money management |

Target uptake ~30m app users |

Beneficiaries 40% |

Avg. annual benefit 12.0m |

10 year cumulative £75 per person |

£9 billion |

|

Eligible population Financial capability |

Target uptake ~25m adults |

Beneficiaries 32% |

Avg. annual benefit 8.0m |

10 year cumulative £100 per person |

£8 billion |

|

Eligible population TOTAL |

Target uptake |

Beneficiaries |

Avg. annual benefit |

10 year cumulative |

£100 billion |

It is assumed that customers’ adoption of digital financial tools will take time, and that the benefits won’t materialise in full from year one.

The modelling assumes a graduated ramp-up over years one through five (from 10% to 80% of target uptake), reaching steady state by year six. Year 1 benefits: ~£3.5 billion. Year 5: ~£9.5 billion. Full scale (Year 6+): ~£10.8 billion per year. (Note: the headline of £100 billion is a central estimate, not an upper limit – a move from 36% to 45% uptake in accessible investing alone adds approximately £5 billion to the ten-year total for that use case.)

The total ten-year benefit of £100 billion equates to approximately £3,500 per benefiting household on average. But for a mortgaged family that pays down debt smartly, the combined benefit can exceed £14,000 over ten years.

Six UK personas

The following personas show how different types of household might benefit from the use cases described in this report, based on the modelling assumptions set out in Appendix A. The estimated benefits are presented in terms of financial value, but the broader significance lies in what that value enables: greater financial security, more informed choices, and improved resilience against unexpected events.

Individual results will vary depending on personal circumstances, the degree of engagement with digital tools, and prevailing market conditions. The personas illustrate potential benefits to individuals in particular situations, and are not recommendations or financial advice.

Estimated 10-year benefit: £5,200

How Anya achieves this benefit

Moving from high-cost to near-prime credit saves her £390/year. Smart debt paydown reduces credit card interest by £180/year. AI budgeting flags £95/month in unnecessary subscriptions. Anya achieves lower borrowing and better budgeting.

Estimated 10-year benefit: £11,400

How Martin achieves this benefit

£25,000 of his cash ISA holdings is redeployed into a balanced investment returning approximately £500/year more relative to cash, with cohort-based guidance on drawdown tax efficiency adding a further £100/year. An insurance review right-sizes his home contents cover and removes a duplicate life policy carried over from an employer group scheme (£140/ year), while digital money management clears around £100/year of previous-employer direct debits now that regular income has stepped down.

Estimated 10-year benefit: £15,400

How Marcus and Sarah achieve this benefit

Digital pre-approval enables swift remortgage, saving £1,900/year. £22,000 in a Cash ISA is moved to a balanced investment portfolio. A life cover gap is identified and duplicate travel insurance is eliminated, saving £140/year. Marcus and Sarah save money on mortgage payments, improve their portfolio returns, and expand their insurance coverage.

Estimated 10-year benefit: £10,800

How Denise achieves this benefit

£45,000 in a cash ISA is redeployed to earn a higher real return. Money management flags recurring charges on expired contracts totalling £34/month. Denise improves the returns on her investments, and benefits from better everyday money management.

Estimated 10-year benefit: £3,400

How Mo achieves this benefit

Open Banking-derived rental and bills data supplement his thin credit file, saving approximately £120/year on borrowing costs. AI-enabled money management flags dormant subscriptions and supports better product selection, saving around £100/year. A modest £50/month contribution into a diversified Stocks and Shares ISA, initiated through digital onboarding, generates an excess real return of approximately £80/year.

Estimated 10-year benefit: £4,100

How Terry achieves this benefit

Open Banking income data enables near-prime credit access. A single-view of four credit products helps him repay them in the optimal order. AI-delivered guidance improves Terry’s understanding of self assessment tax efficiency. Income smoothing tools help manage his irregular cash flow. Terry benefits from simpler management of his credit products, better cash flow, and faster and simpler tax decisions.

These six personas illustrate two patterns: A) Absolute gains are highest for those with more assets – a mortgaged household with investable savings has more resources for digital financial empowerment tools to act on. B) But relative gains – as a proportion of income – are often highest for lower-income households, for whom reducing the cost of debt or unlocking better credit is transformative.

There are three main enablers which allow digital transformation to financially empower consumers, and which span the seven use cases described earlier:

This report has set out to answer a specific question: if the benefits of digitally-enabled financial empowerment were realised at scale across the UK population, what would the total value to consumers be over the next decade?

The analysis shows that the answer is £100 billion.

This answer is derived bottom-up from seven independent use cases, grounded in academic research and national survey data, and applied with conservative assumptions.

That figure breaks down into components that are individually legible and verifiable. £40 billion from shifting investable cash into better-returning portfolios. £15 billion from smarter debt management. £14 billion from timely mortgage switching. £8 billion from unlocking credit for the currently invisible. £6 billion from rightsizing insurance. £9 billion from AI-powered money management. £8 billion from digitally-delivered financial capability.

Each component is a conservative estimate, achievable with technology that already exists or is close to market, and is grounded in published research.

Taken together, these findings highlight a significant opportunity to improve outcomes for millions of people across the nation.

By harnessing the power of data, technology and digital channels – alongside accessible guidance, inclusive services and trusted support – there is a clear path to helping people build financial security, pursue their aspirations, and unlock opportunities to thrive.

"For our customers, financial empowerment is experienced through everyday choices – when digital tools remove friction, provide clarity and support better decisions over time, enabling people to engage with their finances in ways that reflect their own goals and circumstances."

Through simple digital tools, personalised insights and timely guidance, we're helping people make informed decisions every day and take small but meaningful steps toward stronger financial futures.

8 May 2026 | Jas Singh

When people are financially empowered, they are better able to make informed financial decisions. They can spot opportunities, avoid costly mistakes, and make choices that align with their priorities and circumstances.