Sustainability

We have an important role to play in creating a more sustainable and inclusive future.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

We’re supporting the changes that can help make the UK’s houses more energy efficient – and could even contribute to an increase in property value for homeowners.

Making the UK’s homes greener and more energy efficient is an essential step in mitigating the UK’s contribution to climate change. Homes currently account for 23% of the UK’s total carbon dioxide emissions and 35% of energy use. As the demand for high-quality homes is steadily increasing across the nation, the need to decrease the resulting carbon emissions is now urgent.

While newer properties tend to have been designed with more carbon-efficient credentials in mind, there are still steps that owners of older, less energy efficient properties can take to help improve the “greenness” of their house. This can help to decrease a property’s carbon footprint and even save the owner money in the long term. However, homeowners no longer seem to be taking advantage of the available improvement options, with emission reductions from housing having plateaued over the past few years1.

So what’s stopping homeowners from making emission-reducing changes? Research that we carried out with YouGov in August 2021 has shown that, essentially, it’s the perception amongst homeowners that making ‘green’ upgrades would simply cost too much. Almost one in five (17%) of our survey respondents also stated that they wouldn’t increase their budget to make these green home improvements, as they think it wouldn’t save them much on bills.

More than one in five (21%) of our research respondents have had conversations with friends or family about making their home greener, driven primarily by the 25-34 generation (34%). The question is, how do we turn these conversations into actions?

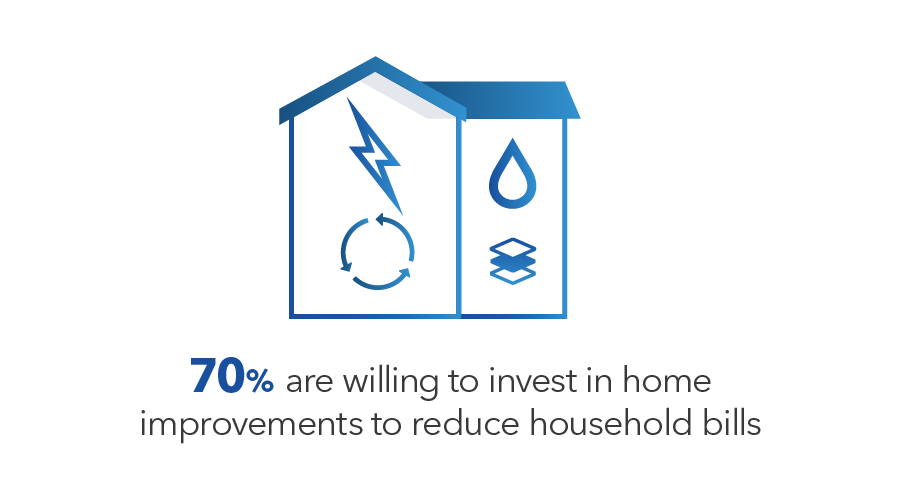

While 66% of respondents said that they’d agree with the idea that they would feel proud of having an environmentally friendly home, it seems that the real motivation behind the majority of property improvements made by owners have been financial, rather than environmental, with 70% of respondents being willing to invest money in home improvements if it meant reducing household bills in the long run.

While making UK homes more carbon efficient has been a top priority for the UK Government, this research has shown that the prospect has become less appealing to homeowners and landlords, due to this perception that making greener improvements will be expensive, with little financial return.

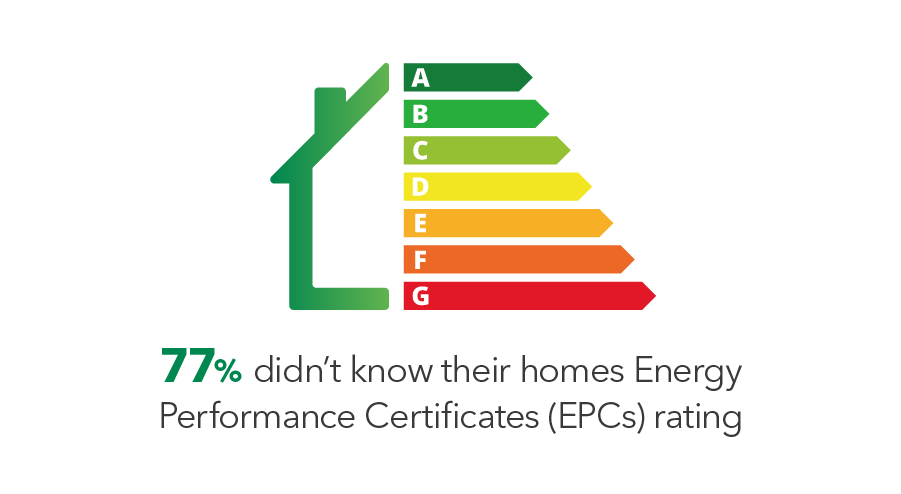

Despite cost being flagged as the main factor in holding homeowners back from making improvements, it’s notable that the majority of respondents were simply unaware of how green their homes were in the first place. 77% of our survey audience didn’t know their home’s Energy Performance Certificates (EPC) rating (more on those later).

Could it be that, rather than cost being the barrier to change as homeowners claim, the real issue is lack of awareness? If so, how do we (the UK Government, finance, energy and property sectors) best come together to inform property owners about their current EPC rating, as well as about the financial – and environmental – benefits of making improvements?

Why do we need a green homes revolution?

As well as being a UK Governmental priority, making greener progress is top of the agenda across most of the UK’s most profitable industries. From the upcoming switch over to electric vehicles in 2030 in the transport and motor sector, to the emphasis on investment in renewable energy, it’s clear to see that going green isn’t only the right thing to do for the planet – it also makes good business sense.

The transition to a low carbon economy – a ‘green’ economy – will support the UK’s recovery and promote long-term prosperity, while helping to make our planet more resilient and driving inclusive growth. Housing, of course, plays a vital role in this.

What makes a home "green"?

In the UK, Energy Performance Certificates (EPCs) are an important part of buying, selling and renting homes. They show a property’s energy efficiency based on:

Properties are rated on a colour-coded scale (A-G). A is the most efficient with the cheapest energy bills and the lowest impact on the environment. EPC ratings (A-G) are based on the Energy Efficiency Index, roughly a scale from 1-100. Homes that rank from a C grade and upwards would be considered ‘green’.

Some home features that would help to contribute to a higher (A-C) EPC rating include:

Does making a home greener increase the property value?

So are property owners right? Would the costs of making energy efficient changes to their homes be more than the return value? In order to determine if greener, more energy-efficient homes are really worth more, Lloyds Banking Group ran an advanced analysis to define the “Green Homes Premium”; the average added-value of more sustainable, lower-impact properties in England and Wales.

We conducted correlative analysis to see if there was a link between changes in the average energy efficiency (EPC rating) in a Local Authority District in a given year, and the average property prices in the same Local Authority in the following year.

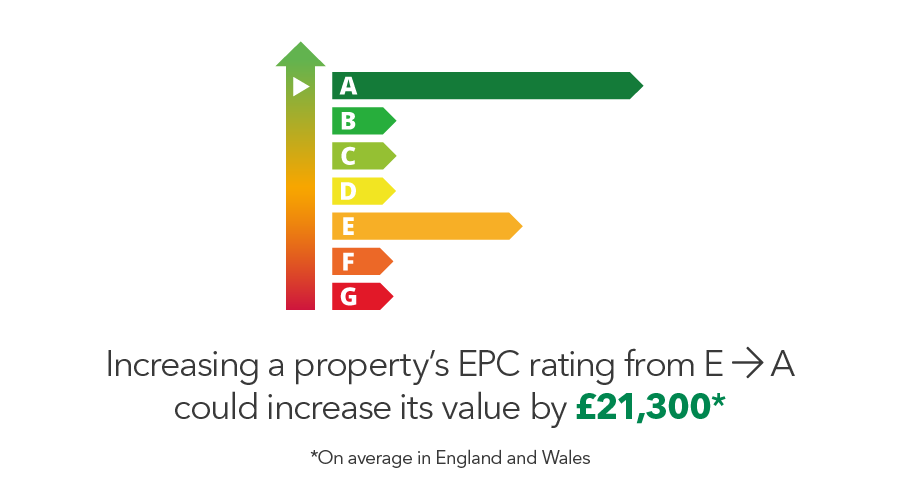

Overall, our research showed that there was a correlation between “greener,” more energy-efficient homes being worth more than homes with a lower EPC rating. Across all Local Authority Districts in England and Wales, we found that there’s an increase in property prices of £474, per one point increase in energy efficiency, on a scale from roughly from 1-100. This means that increasing a property’s EPC rating from E > A would, on average, increase its value by £21,300, and there are even greater returns on improving highly energy-inefficient properties.

However, this “Green Homes Premium” shows diminishing returns as energy-efficiency increases. For example, there is greater value in upgrading wasteful, energy-inefficient homes (e.g. from G > F) than already highly energy-efficient homes (e.g. from B > A). Moving a property from a B rating to an A can be challenging - and expensive. There can be far more value (and potential cost savings) for those living in lower-rated homes to make green updates.

Location makes a difference too, as the “Green Homes Premium” is worth more in some regions of England and Wales than in others. Property owners in the South East, East of England, West Midlands, Yorkshire and Humber, and the South West could add even more value to their homes with EPC improvements, compared to those in the North East, North West, East Midlands, and Wales.

We also see green home “hot” and “cold” spots across the regions too, with London, the North East and South East boasting the highest volume of green homes, while Wales and the South West have the lowest number of energy efficient homes.

Our “Green Homes Premium” research tallies up with our YouGov survey findings as, despite the majority of our survey recipients not knowing their own properties EPC rating, 42% of them rated it as an important factor when choosing their current home.

Property energy efficiency is a factor that is becoming increasingly more important to businesses, as well as to homeowners themselves. While there are specialist “green mortgages” and grants on the market (our housing brand Halifax currently offers one) EPC rating of a property is likely to become ever more important in the mortgage market, which is why it’s something we’re looking to capture as part of the mortgage application.

What are the greener housing changes that homeowners and landlords can make for the highest returns?

Homeowners who want to reduce their carbon footprint are often told about the quick wins and lifestyle changes that can be made immediately to make a home more energy efficient, such as:

But what about the bigger changes that require more commitment and, often, financial investment? Energy-saving LED lighting is the most common improvement that our survey respondents have made (60%), and this is driven by a desire to save money on bills (39%). Meanwhile, the most common change that respondents would be willing to make in order to improve the value of their home is installing a boiler upgrade (7%).

But there still seems to be hesitation when it comes to uptake of these green improvements. It may be that the relevant industries and UK Government bodies still need to work together more efficiently to better communicate with homeowners about the potential returns of any greening investment that they make – and where to start.

Tools like the Halifax Green Living hub can help customers (and homeowners in general) get a better sense of their home’s carbon credentials, the opportunity to apply for a Green Living Reward, as well as information on which changes can have the biggest impact on their EPC rating. While these tools are signposted to Halifax customers, there is more that could be done to make access to this information – and equivalent tools – more widely available to homeowners across the UK who are with other providers.

How is Lloyds Banking Group helping to make home “greener”?

Helping to make the nation’s homes greener is a priority for us at Lloyds Banking Group, and this year we’ve committed to provide £1.5 billion of new funding support, including £500 million in ESG-linked funding, in support of the social housing sector.

We’re also considering the environmental impacts of our products and partners where possible. For example, Halifax’s green mortgage cashback scheme offers £250 to those buying homes with an EPC rating of A or B, and our Halifax home insurance customers making a claim for a leak or water damage will be given the option of downloading the My Carbon Manager app, which shows people how to make their lives more energy efficient.

Our commercial customers have access to Lloyds Bank’s Green Buildings Tool, so commercial landlords will be able to use the calculator to identify, evaluate and understand the estimated outcomes of potential investments to make a property more sustainable and energy efficient.

Halifax customers could also be entitled to a green living reward if they’ve made certain energy efficient improvements to their home, such as installing low carbon heating or insulation. Our free Homes Energy Saving Tool can be used by anyone, so homeowners can calculate how carbon efficient their home really is, as well as where they could make changes – and savings. The tool also gives a suggestion of what a properties current EPC rating is, which could help the 77% of homeowners who are currently unsure of their properties carbon footprint.

There’s still a lot to do to help to reduce the emission contributions from residential properties. But if our industry, the UK Government, and the energy and wider housing sectors can work together effectively, then we have an opportunity to provide homeowners the right information and support to make their homes more carbon efficient.

1UK housing: Fit for the future? - Climate Change Committee (theccc.org.uk)

The Housing Growth Partnership (HGP), a joint venture between Lloyds Banking Group and Homes England. We're working together to help address the need for new homes across the UK.

The next decade will be crucial for protecting the planet for future generations, and financial services has a critical role to play by helping to incentivise the financing of the changes required.

What can we expect from the housing market in 2025?

Popular topics you might be interested in