Sustainability

We have an important role to play in creating a more sustainable and inclusive future.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

We have an important role to play in creating a more sustainable and inclusive future.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

We put you first, so you can put our customers first.

Our report provides an update on how we are Helping Britain Prosper in a way that delivers long-term profit and returns.

Disclosures relating to our strategic, financial, operational, environmental and social performance.

See all the key dates in the financial year.

Higher, more sustainable returns as we continue to Help Britain Prosper.

With hubs across the UK, there's a place for you.

We're searching for the best talent to join us in Leeds.

Join us as we explore new ideas and technologies to reshape the world of finance.

Catherine Rutter, Group Customer Vulnerability Director, looks at the importance of ensuring customers in vulnerable circumstances are supported in the best ways that suit their needs.

According to the Financial Conduct Authority definition, “A vulnerable customer is someone who, due to their personal circumstance, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care.”

I think it’s really important to recognise that anyone can become vulnerable at any time, something that was made very clear during the pandemic which shone a light on vulnerable circumstances.

For instance, we’ve seen an increase in people accessing online domestic abuse and mental health support, and sadly many more people have suffered a bereavement. For some, it’s also brought to light vulnerabilities related to finances, with more people losing their jobs or seeing their income reduced. Supporting customers in vulnerable circumstances was important before the pandemic hit, and it will continue to be a priority as we all transition to life after it.

In October 2020, 53% of UK adults had characteristics of vulnerability, up from 46% in February 2020

FCA Financial Lives Survey 2020

The term “vulnerability” encapsulates the various circumstances our customers can face, and risks of financial harm that we work to mitigate for them. However, it’s not a word that people like to identify with or sometimes even recognise in themselves, and that’s okay. What most customers will identify with, is what support they need in order to manage their day-to-day banking.

This is why we focus on understanding those needs, supporting our colleagues to have empathetic conversations which in turn makes it easier for customers to tell us what they need, and to provide them with the tools, flexibility and support to address them.

We continuously work to ensure we can incorporate vulnerability considerations into all that we do, whether it’s by designing inclusive products, communications, treatments or channels. We aim to support those already living in vulnerable circumstances, and to be ready to make things easier for anyone who falls into those situations, and where we can, help prevent them from doing so.

As a financial services provider, we recognise that vulnerability is so broad; we’re not the experts, so sometimes we need a little help from those who are.

Working closely with third party organisations is invaluable to the Group and in Group Customer Vulnerability we partner a number of different charities and other groups to really understand the challenges facing some of our customers with additional needs.

They’re working every day supporting people with vulnerabilities in areas ranging from gambling and mental health to digital exclusion. They provide invaluable feedback as we develop products and services. Would this work? What could we do better? What barriers might we have missed?

We signpost customers to them for the emotional and additional practical support that we, as Financial Services providers, can’t offer. These relationships help us get to the right solutions and work both ways, as we also help charities understand our processes and the support available to their service users.

Recognising that we’re not the experts in Mental Health, we’ve developed a strong relationship with the Money and Mental Health Policy Institute. They’ve shared invaluable insights with us into the links between Mental Health and money management, including:

More than one in five (22%) people with a recent mental health problem say they have had a panic attack as a result of dealing with an essential services provider.

To support essential service providers, such as banks, energy or broadband suppliers and water companies to better understand and address the challenges that customers with mental health problems face using their services, Money and Mental Health created their Mental Health Accessible programme, which reviews how accessible these services are for customers with mental health problems

I’m pleased to be able to say that in September this year, Halifax and Bank of Scotland became the second and third firms to receive the accreditation, after Lloyds Bank received the first accreditation in 2020. Based on recommendations from Money and Mental Health, we’ve taken significant steps across all three brands to ensure our services are more accessible and supportive for vulnerable customers, including:

I’m so delighted that in recognition of these steps, Money and Mental Health has awarded Lloyds Bank, Halifax and Bank of Scotland an ‘Essentials’ rating, the first of three levels which firms can achieve when taking part in the Mental Health Accessible programme.

We recognise though that there’s more work to do and Money and Mental Health has given Halifax and Bank of Scotland an action plan to help them make further improvements — for example, making it easier for colleagues to support customers with mental health conditions by providing them with additional tools and information.

In addition, Money and Mental Health has also renewed Lloyds Bank’s “Essentials” accreditation for another year, to reflect the bank’s continued commitment to improving the accessibility of its services.

Helen Undy, Chief Executive of the Money and Mental Health Policy Institute, said: “Dealing with essential services providers can be difficult for anyone. But for the 12 million people across the UK experiencing mental health problems, it can feel like an impossible task. This leaves people effectively locked out of services which are critical for everyday life and can create serious distress for people who are already struggling”

Director, Customer Vulnerability team

Catherine Rutter is the Director of Lloyds Banking Group’s Customer Vulnerability team, who are responsible for driving improved experiences and fair outcomes for customers in vulnerable circumstances. Gaining insight from partners, the team works to further the Group’s understanding of vulnerability whilst developing plans, priorities and guidance to better support customers in a way that meets their individual needs.

We launched our partnership with Mental Health UK in January 2017, with the aim of raising £4 million over two years.

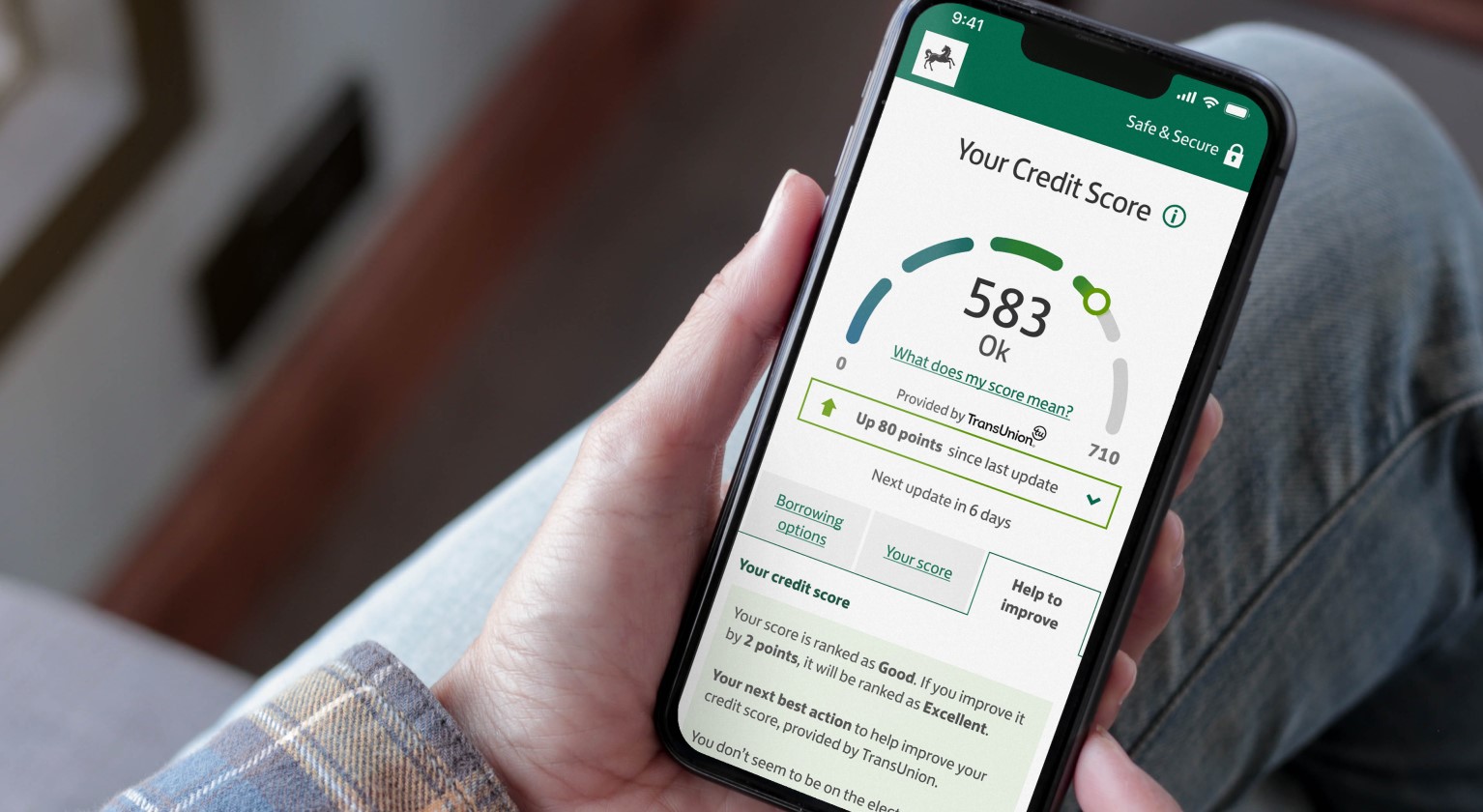

Your Credit Score is helping customers take control of their money, build their financial confidence, and even tackle fraud.

Popular topics you might be interested in